Business Credit Card Fraud: Part 2 (Fraud Prevention Guide)

.jpeg)

TLDR;

- Business credit card fraud is harder to detect than personal card fraud because multiple employees use cards, limits are higher, vendor access is widely shared, and reconciliation often happens only once a month

- The five biggest fraud risks are card-not-present (CNP) fraud, account takeover (ATO), business email compromise (BEC), employee expense manipulation, and fake vendor fraud

- The most common warning signs include charges just below approval thresholds, unusual merchant categories or locations, repeated small transactions, missing receipts, and recurring charges from unknown vendors

- Hotel credit card authorization forms are one of the largest overlooked fraud risks because they expose full card details through email or fax and allow post-checkout charges long after the stay ends

- Fraud prevention is primarily about reducing exposure before unauthorized charges happen, not just recovering money after fraud appears on the statement

Most companies think about fraud only after unauthorized charges appear on the statement. By then, the damage is already done: cards are frozen, employees are blocked from making payments, finance teams are buried in reconciliation work, and recovery timelines stretch for weeks or months.

The reality is that most business credit card fraud is preventable. Fraud rarely succeeds because attackers are exceptionally sophisticated. It succeeds because controls were missing, card details were exposed in too many places, approvals were weak, or suspicious activity wasn't caught quickly enough.

Business card programs create a larger attack surface than personal cards by default. Multiple employees use cards, limits are higher, vendors store payment credentials across systems, and monthly reconciliation delays detection. That combination makes prevention far more important than recovery.

This guide breaks down the most common types of business credit card fraud, the warning signs companies miss, and the exact controls finance teams use to reduce fraud risk before unauthorized charges happen. It also covers one of the most overlooked exposure points in corporate travel: hotel credit card authorization forms and why virtual cards are rapidly replacing them.

What Is Business Credit Card Fraud and Why It's Harder to Catch Than Personal Card Fraud

Business credit card fraud is unauthorized use of a company card, whether by external attackers or by employees misusing cards they were authorized to hold. The legal protections look similar to personal cards on paper, but detection is harder for reasons that don't apply to consumer cards.

- Multiple users: A personal card has one or two cardholders who recognize their own transactions. A company card program has 50 or 500 cardholders, and no single person is reviewing every charge.

- Higher limits: Personal cards typically have limits in the low five figures. Corporate cards routinely have limits in the six figures. The dollar-per-transaction ceiling for "looks normal" is much higher, which means individual fraudulent charges hide more easily inside the noise.

- Shared access patterns: Vendor portals, hotel CC authorization forms, recurring SaaS subscriptions, and travel booking sites all store corporate card details in multiple places by design. Personal cards typically aren't shared this widely.

- Monthly reconciliation lag: Most finance teams reconcile cards monthly, not weekly. That creates a 30-day blind spot where fraudulent activity can run before anyone notices.

The Association of Certified Fraud Examiners (ACFE) reports that organizations lose about 5 percent of revenue to fraud annually, with median losses higher in organizations that lack basic spend controls. Detection lag is the other half of the problem: ACFE's data shows internal occupational fraud typically goes undetected for around 12 months on average, longer for the harder-to-detect schemes.

Business vs. personal fraud at a glance:

5 Types of Business Credit Card Fraud and How Each One Enters Your System

External fraud and internal fraud each split into specific categories. Knowing which type you're dealing with changes the right controls and the right response.

1. Card-Not-Present (CNP) Fraud

Stolen card details used online, over the phone, or on hotel booking forms where the physical card isn't required. CNP is the highest-growth fraud vector as remote work and online vendor payments expand the surface area. The card number enters the fraudster's hands through a data breach, a phishing campaign, or a dark-web purchase of stolen credentials.

CNP fraud is what most virtual-card and merchant-category-control programs are designed to prevent. The control logic is: even if the number is compromised, restrict where and how much it can transact.

2. Account Takeover (ATO)

A fraudster gains legitimate credentials (login, password, MFA bypass) and operates inside the card program as if they were the cardholder or an admin. ATO is the hardest type to detect because the activity looks like normal access from a known user.

Javelin Strategy & Research has tracked rising ATO losses across consumer and business accounts for several years. The control logic against ATO is layered authentication (MFA on every privileged action, not just login) plus behavioral anomaly detection (the system notices when the "user" is suddenly logging in from a new device, location, or in a new pattern).

3. Business Email Compromise (BEC)

An attacker impersonates an executive, finance manager, or vendor and authorizes fraudulent card charges or wire transfers through legitimate-looking email. The FBI's IC3 reports BEC as one of the highest-loss fraud categories, with median per-incident losses well into five figures and aggregate annual losses in the billions.

BEC typically isn't detected until the real executive or vendor is contacted directly. The control logic is approval workflows for transactions above a threshold (a second human must authorize before the charge processes), plus out-of-band verification for any payment-detail change (call the vendor at a known number to confirm, don't reply to the email).

4. Employee Expense Manipulation

Falsified receipts, inflated amounts, personal costs submitted as legitimate business expenses, or duplicate submissions. ACFE's Report to the Nations consistently shows expense reimbursement schemes account for a meaningful share of all occupational fraud cases, with a long median detection lag because the individual amounts stay small enough to avoid scrutiny.

The control logic is real-time receipt matching (no documentation, no approval), random sampling audits, and pattern analysis on submitter behavior (the same employee submitting receipts from unusual merchants or with rounded-amount patterns).

5. Fake Vendor Fraud

Small recurring charges from fictitious vendors designed to stay below review thresholds. The fraudster sets up a vendor that looks legitimate, charges small amounts month after month, and bets that nobody will audit it for a year or two. Most fake-vendor schemes are discovered during annual audits rather than monthly reviews.

The control logic is vendor pre-approval (no new vendor receives a charge without onboarding review), recurring-charge audits (every recurring charge gets a quarterly check), and merchant category enforcement (limit which categories a given card can transact in).

Warning Signs You're Already Dealing With Fraud

Eight signals show up repeatedly in fraud investigations after the fact. Spotting one or two isn't proof of fraud, but spotting three or more in the same time window is a signal worth a closer look.

- Charges just below your approval threshold: Classic structuring behavior, designed to slip under the review limit

- Transactions outside normal business hours, geography, or merchant categories: A card that normally transacts at airlines and hotels suddenly buying electronics at 2am is a flag

- Multiple charges to the same vendor in a short window: Card testing pattern, fraudsters confirming the card is live before larger charges

- Receipts submitted late, missing, or with amounts that don't match the charge: The single most reliable signal of employee expense fraud

- Former employee cards still showing active transactions: Offboarding gap, easily missed

- Sudden increase in declined transactions on a card: Often means fraudsters are testing variations of a card number they have partial details on

- Unrecognized recurring charges from vendors you didn't onboard: Fake vendor pattern

- Employees who consistently delay or resist submitting receipts: Not always fraud, but always worth a conversation

If you see two or more of these on the same card in the same week, treat it as a fraud investigation, not a routine review.

The Corporate Travel Fraud Gap: What Most Fraud Guides Don't Cover

The fraud surface that almost no guide addresses is corporate travel payment, specifically hotel credit card authorization forms. This is where many real-world business card breaches actually start.

1. Why Hotel Payments Are Your Highest Card-Not-Present Fraud Surface

Hotel credit card authorization forms transmit full card details (number, expiration, CVV, billing address) via email or fax. Unencrypted email is interceptable at every hop. Faxes are not interceptable in the same way but are stored as paper documents at the property, accessible to front-desk staff with no auditable accountability trail.

High-limit corporate cards authorized for hotel stays expose the entire card limit, not just the booking amount. The hotel keeps the card on file. Authorized for $400 a night, the property has the credentials to attempt charges far beyond that.

Post-checkout charges added without authorization are a known pattern: minibar disputes, damage claims, parking, or "incidental" charges processed days or weeks after the guest departs, when the booking team has moved on to other reservations and the company isn't actively monitoring the card.

2. How Fraudsters Exploit CC Authorization Forms Specifically

- Phishing fake hotel requests: A fraudster impersonates the hotel asking the company to re-send the CC authorization form for a "system update" or "form re-submission." The booking looks real because the fraudster has scraped public booking details. The form is sent to an attacker-controlled email and the card details are harvested.

- Email interception: Full card details in plain text in an email chain, visible to anyone with access to the inbox or to anyone who intercepts the message in transit. Mid-sized businesses often don't run mail-encryption policies that would protect this.

- Insider misuse: Hotel staff with access to the paper or stored copy of the authorization form. Most properties have weak audit trails on who accesses what, especially after a guest has checked out.

- Post-checkout charges: Once a card is on file with a property, the property's billing system can attempt charges for weeks. If your card and the booking team haven't reconciled the stay, those late charges are easy to miss.

Why High-Limit Corporate Cards Shouldn't Be Used for Hotel Auth Forms

Sending your primary corporate card to a hotel exposes your entire credit limit for the duration of the stay and beyond. A single compromised hotel form gives access to the card that every other company expense runs through, including subscriptions, vendor payments, and travel for everyone else.

The recovery cost isn't just the fraud amount. It's the card freeze (every employee on that card needs a new one), the rebooking disruption (every hotel and vendor with the old card on file needs updates), and the reconciliation time finance spends matching old transactions to new card numbers.

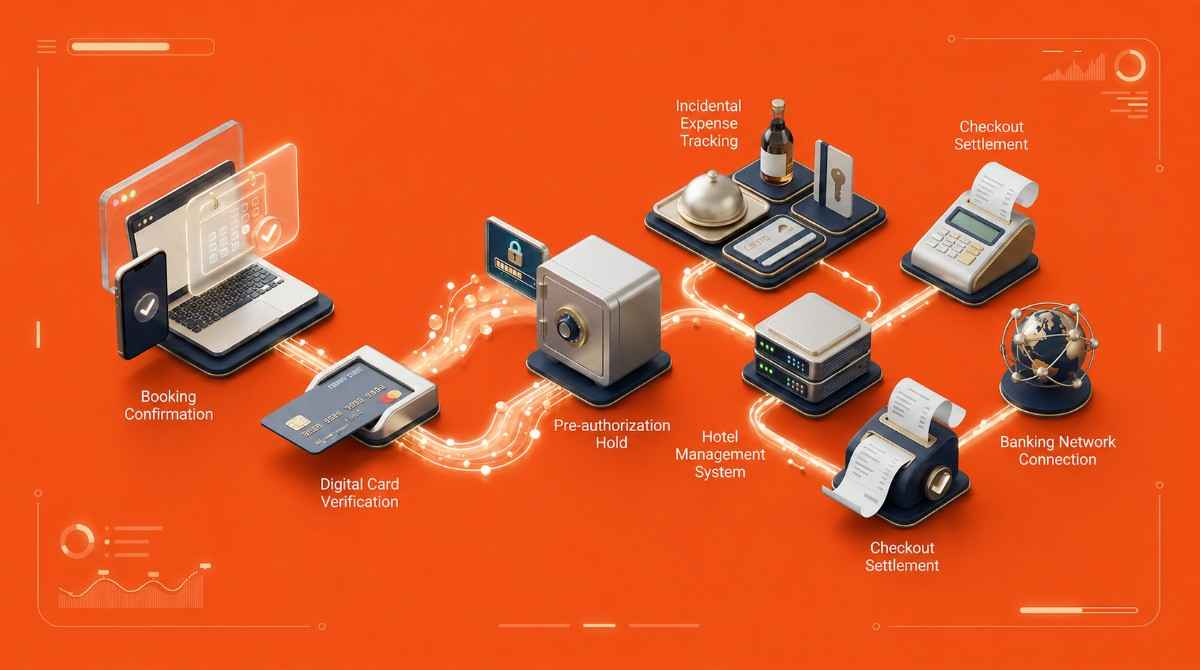

The Virtual Card Fix

A virtual card number is generated specifically for a single booking, pre-approved for the exact amount of that booking, and automatically deactivates after checkout. Card details go directly to the hotel through the booking system rather than through email or fax. Even if intercepted, the virtual number is single-use and useless for any other transaction.

ITILITE issues virtual cards on every hotel booking through the platform, payment details confirmed with the property before arrival, no CC authorization form required. The fraud surface from the form process is eliminated structurally rather than monitored after the fact.

What Security Features Should Your Corporate Card Platform Have?

Use the checklist below as an evaluation framework when comparing platforms. Each item maps to a specific fraud type or detection delay. The platforms that ship all of these by default are the ones that produce the fewest fraud cases per dollar of spend.

- Real-time transaction alerts configurable by amount, location, merchant category, and time of day

- Role-based spending limits by employee and transaction type

- Merchant category code (MCC) restrictions

- Virtual card issuance

- Instant freeze and deactivation, including automated deactivation triggered by offboarding

- AI anomaly detection

- Receipt matching within 48 hours

- Complete audit trail

ITILITE delivers all of these across corporate cards plus the hotel virtual-card workflow that removes the travel fraud surface entirely.

Prevention Controls Mapped to Each Fraud Type

The table below gives a one-control answer to each fraud type. Match the type you're worried about to the primary control, and the rationale tells you why that specific control works.

If you only implement three of the six, the highest-ROI picks are virtual cards per transaction, approval workflows for large transactions, and receipt documentation within 48 hours. Those three close the majority of the typical attack surface.

FAQ

How is employee expense fraud different from external card fraud?

External fraud is unauthorized use by someone outside the company; employee fraud is misuse by an authorized cardholder. External fraud is handled through the card issuer under TILA. Employee fraud is an employment matter handled through HR, legal counsel, internal investigation, and potentially insurance and law enforcement. Mixing the two playbooks weakens both cases.

How do virtual cards prevent business credit card fraud?

A virtual card is a unique card number generated for a specific transaction or vendor with a capped amount and an expiration. Even if the number is compromised, it can't be used anywhere else or for any other amount. Virtual cards close the entire card-not-present fraud surface, including hotel booking exposure where physical CC authorization forms transmit card details unencrypted.

Can a hotel commit credit card fraud using an authorization form?

Hotels rarely commit fraud directly, but the CC authorization form is a leak point. Insiders with access to the form, intercepted emails containing card details, and post-checkout charges added without authorization all originate from the form process. Virtual cards eliminate the form entirely by sending payment details directly through the booking system.

What are the most common warning signs of corporate card fraud?

Charges just below approval thresholds (structuring), transactions outside normal hours or locations, multiple charges to the same vendor in a short window, receipts that don't match charges, former-employee cards still active, sudden spikes in declined transactions, and unrecognized recurring charges. Two or more signals on the same card in the same week warrants a fraud investigation.

How do I build fraud prevention into my corporate card policy?

Cover six elements: spending limits by role (not blanket limits), documentation requirements with a 7 to 14 day submission deadline, approval thresholds with named approvers and response times, an offboarding checklist that deactivates cards same-day, quarterly access reviews of limits and users, and named consequences for violations stated in the policy before anyone receives a card.

Ardra is a Content Strategy Manager at ITILITE with 6+ years of experience in travel and SaaS content. She holds a Master’s degree in Political Science from Lady Shri Ram College for Women and transitioned from academic research and travel content into SaaS content strategy.

She previously worked with JustWravel, where she focused on travel storytelling and digital content. Today, she specializes in SEO and AEO-driven content strategies that help businesses simplify complex travel and expense workflows into search-optimized narratives.

When she’s not working, Ardra is usually reading or watching films.

The safest corporate card is the one vendors never store

A fully integrated corporate travel management software that dramatically reduces spends while improving user experience

.jpeg)

.jpeg)

.jpeg)

%20(1).png)

%20(1).png)

.jpeg)

.jpeg)

.webp)

.jpeg)

.jpeg)

.webp)

.png)