It’s Sunday afternoon. A travel manager at a medical staffing company has just booked a hotel for a traveling nurse whose check-in is Monday morning. She now has roughly 18 hours to call the hotel, wait for a confirmation email, fill out a credit card authorization form, and fax it back, then hope the front desk staff finds it when the nurse arrives. She does this every single week, for every single placement.

That scenario is not unusual. It is the default state of corporate hotel payment in 2026. And it raises a question worth answering properly: what is actually happening, mechanically, financially, and legally, when a hotel asks for credit card authorization, and why does the process break so consistently?

This article answers that question in full. We start with the universal mechanics every card transaction shares, move through authorization holds and their real-world implications, and then explain exactly why corporate travel makes all of it harder.

What Is Credit Card Authorization?

Credit card authorization is an approval issued by the card’s issuing bank confirming that the card is valid and that sufficient funds or credit exist to cover a transaction. It is not a charge. No money moves. It is a temporary hold, a reservation of funds, that allows the merchant to proceed with confidence that they will be paid.

The word “authorization” does double duty. As a noun, it refers to the approval itself: “We have authorization for this purchase.” As a verb, it describes the act of requesting that approval: “We are in the process of authorizing this transaction.” The distinction matters because the authorization can expire before funds are ever captured, a detail that creates real problems in hotel and travel contexts, covered below.

Four parties are involved in every authorization, regardless of industry:

- Cardholder: The individual whose card is being used for payment.

- Merchant: The business accepting the card, a hotel, airline, vendor, or retailer.

- Acquiring bank (acquirer): The merchant’s bank. It processes card payments on behalf of the merchant and communicates with the card network on their behalf.

- Card network: Visa, Mastercard, American Express, or Discover. The network routes the authorization request between the acquirer and the issuing bank.

- Issuing bank (issuer): The cardholder’s bank or credit union. It holds the account, evaluates the request, and approves or declines the transaction.

Every single one of the more than one billion credit card transactions processed globally each day passes through this chain (Stripe, 2024).

Understanding the chain is what makes the failure points in corporate travel legible.

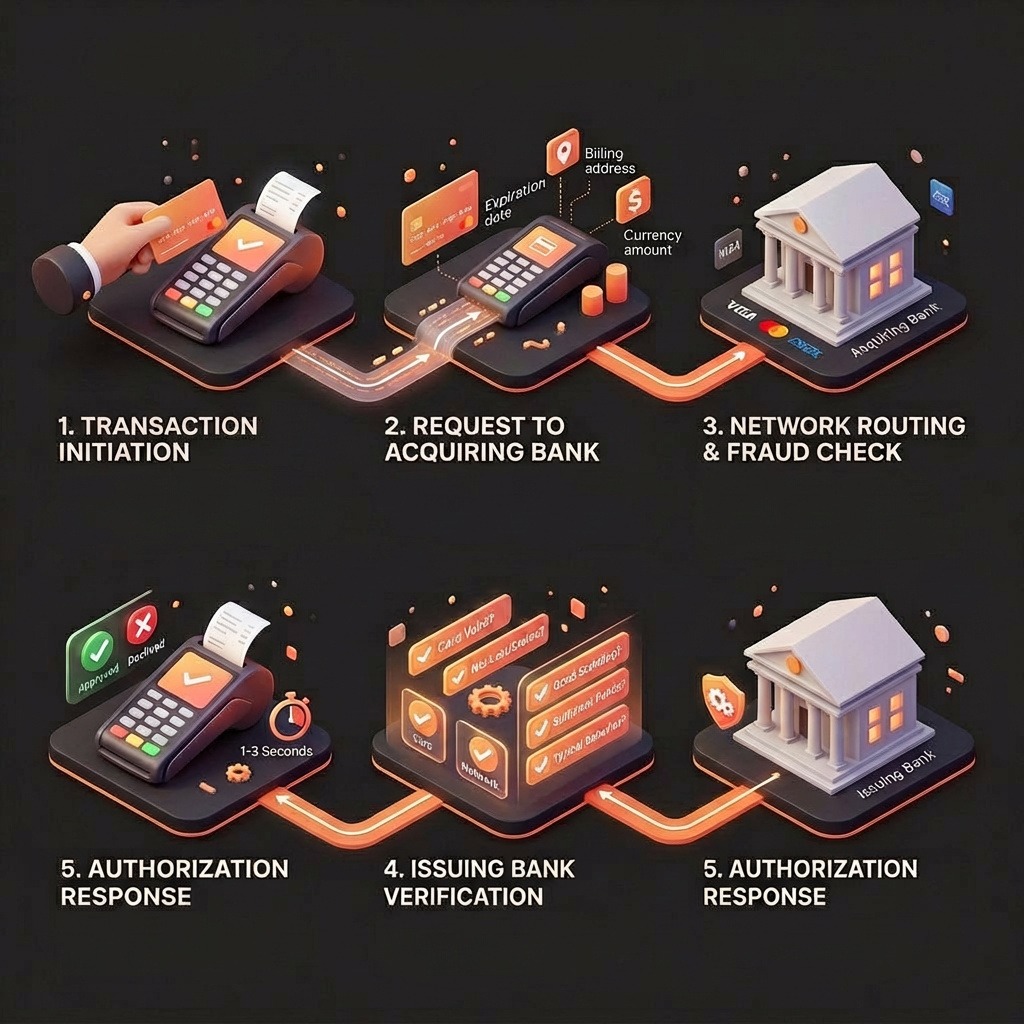

How the Credit Card Authorization Process Works (Step by Step)

The mechanics are consistent whether the purchase is a cup of coffee or a three-week hotel stay. Here is the exact sequence:

- The cardholder presents a card at point of sale or submits card details online. This initiates the transaction and triggers the authorization request.

- The merchant’s POS system or payment gateway sends an authorization request to the acquiring bank. This request includes the card number, expiration date, billing address, and the transaction amount.

- The acquiring bank routes the request through the card network to the issuing bank. Visa, Mastercard, or Amex acts as the communication layer here, it is not a passive pipe. Networks apply their own fraud rules before the request ever reaches the issuer.

- The issuing bank runs its checks. Is the card valid and not reported lost or stolen? Is the account in good standing? Are sufficient funds or available credit present? Does the transaction pattern match the cardholder’s typical behavior?

- The issuing bank returns an approval or decline code. The card network and acquirer relay that response back to the merchant’s terminal, typically in 1–3 seconds for in-person transactions.

A critical clarification: no money transfers into the merchant’s account during authorization. This is the most commonly misunderstood aspect of the process. What authorization does is place a hold, a reservation. on the cardholder’s available balance. The actual movement of funds happens later, during a separate step called capture and settlement, typically within 24–72 hours after the merchant finalizes the transaction. If the merchant never captures the authorization, the hold expires and the reserved funds are released automatically.

Authorization Hold, What They Are & How Long They Last

An authorization hold is a temporary reservation of funds on a cardholder’s account. It reduces available balance immediately, but it does not complete a fund transfer. The merchant has not been paid. The cardholder has not been charged. A hold exists in a financial limbo between those two states.

Hold durations vary by card type and merchant category. As a general range:

- Most authorization lasts 1–30 days depending on the issuing bank and card network rules.

- Visa holds are commonly released within 7 days if no capture occurs.

- Other card types may carry holds of 20–30 days before automatic release.

Industries that routinely place pre-authorization holds include:

- Hotels: Pre-auth at check-in for room rate plus estimated incidentals.

- Car rental companies: Hold for estimated rental cost plus damage deposit.

- Gas stations: Pre-auth of a fixed amount (commonly $100–$175) before the actual fuel total is known.

- Restaurants: Pre-auth may include an estimated tip amount.

- Online marketplaces: Hold placed at order, captured at shipment.

The practical risk: if a merchant pre-authorizes a higher amount than the final charge (common in hotels, which estimate incidentals), the cardholder’s available balance reflects the higher hold amount until settlement resolves it. For travelers on tight per diem budgets, this creates real problems.

What happens if the merchant never captures? The hold expires on its own timeline, but the cardholder has no control over when that happens. Travelers sometimes see funds “tied up” for days after checkout with no charge ever processed. This is one of the most consistent sources of traveler frustration surfaced in practitioner discussions, and it stems entirely from merchants failing to finalize captures promptly.

Credit Card Authorization in Corporate Travel & Why the Process Gets Complicated

The five-step flow described above assumes one thing: the cardholder is present at the time of transaction. Corporate travel consistently breaks that assumption. When a company centralizes payment on a single card held by a finance team, a virtual card issued by a travel platform, or a lodge card account, the person checking in has no card to present. The hotel still needs payment authorization. The result is a category of workarounds that are manual, error-prone, and structurally fragile.

1. The Cardholder Isn’t at the Property

In corporate travel, the card used to guarantee a booking is rarely the card the traveler carries. Companies route hotel payments through centralized corporate cards, virtual cards, or lodge accounts to reduce reimbursement cycles and limit card proliferation. A common goal cited by finance teams is moving away from reimbursements entirely, reducing the number of physical corporate cards in circulation while still giving travelers frictionless access to paid accommodations.

Hotels solve the card-not-present problem with a credit card authorization (CCA) form, a document that grants the property explicit written permission to charge a specific card that will not be physically present at check-in. Filling out, transmitting, and confirming receipt of that form is the manual process that generates the most operational burden for travel managers at mid-size firms. It is not an edge case. Across industries from medical staffing to higher education to enterprise procurement, the CCA form is the standard instrument for centralized hotel payment.

2. Virtual Cards Introduce a Timing Risk Window

When virtual cards are used, single-use card numbers issued by a travel platform or corporate card provider for a specific booking, the hotel must receive the card details before the traveler arrives. The standard window for virtual card transmission is 24–48 hours prior to check-in. That window is not a workflow inconvenience. It is a risk window.

Any booking made within that 24–48 hour window, a same-day trip, an itinerary change, a Sunday afternoon booking for Monday morning, arrives at the hotel with authorization details that may not yet be transmitted or processed. Weekend travel is structurally vulnerable: bookings made Friday afternoon fall into a window where hotel administrative staff may not be available to receive and log authorization details before Monday check-in. Itinerary changes compound the problem because the original virtual card may be invalid for the revised stay dates or property.

Tools like ITILITE allow travel managers to issue virtual cards and transmit authorization details directly to hotels within the booking workflow, reducing the manual handoff that creates this window.

3. Hotel-Side Reception Remains Inconsistent

Even when a company sends a CCA form correctly, on time, and with complete card details, execution depends on the front desk staff finding it and processing it correctly at check-in. This is the failure point that surprises most travel managers: they solve the process on their end and still get calls from travelers denied at check-in because the authorization was not located.

Faxes get lost in incoming queues. Emails arrive in generic hotel inboxes and are not forwarded to the front desk. Authorization forms submitted through hotel-managed portals require property-by-property account setup. The failure mode is not the sender, it is the receiving end. This is why even well-designed corporate authorization processes require a manual confirmation loop: send, confirm receipt, check again at check-in.

Why Credit Card Authorization Forms Still Exist (and Why Fax Hasn’t Died)

The persistence of fax in hotel payment authorization is not nostalgia. It is institutional inertia with a specific origin. Many hotel properties, particularly independent hotels and older branded properties, built their back-office workflows around fax as the default transmission method for card-not-present authorizations. The form itself is a legal instrument: it captures cardholder consent in writing, with a signature, for a specific charge. Hotels require it because it provides paper documentation of authorization in the event of a dispute or chargeback.

Email has largely replaced fax at larger chains, and some properties now use secure digital portals. But the fundamental instrument, a signed document granting charge permission, has not changed. What has changed is the proliferation of submission methods (fax, email, Canary, internal platform, portal), which creates a different problem: travel managers must track not just whether authorization was sent, but which method each property accepts and whether that method was used correctly.

| Transmission Method | Common For | Key Risk |

|---|---|---|

| Fax | Independent hotels, older branded properties | Lost in incoming queue; no delivery confirmation |

| Mid-scale and upscale chains | Arrives in generic inbox; not forwarded to front desk | |

| Hotel portal (Canary, etc.) | Larger branded properties with digital workflows | Requires property-by-property setup; traveler must still confirm on arrival |

| On-site manual form | Fallback when other methods fail | Delays check-in; requires travel manager to provide card details in real time |

Why Card Authorization Fails & What It Means at Check-In

Authorization declines are not always about insufficient funds. Understanding the actual reasons helps travel managers troubleshoot faster when a traveler calls from a hotel lobby.

- Expired or incorrectly entered card details: Virtual cards with tightly scoped validity windows are particularly vulnerable if the booking dates shift.

- Velocity flags: Issuers flag accounts that show rapid-fire authorizations, a pattern common when multiple travelers book the same day under a single corporate card.

- Merchant category mismatch: Some virtual cards are scoped to specific merchant category codes (MCCs). A card issued for airline charges may decline at a hotel terminal.

- Amount variance: If the hotel attempts to pre-authorize an amount larger than the card’s approved limit (common with incidental holds), the authorization fails even if the room rate itself is within scope.

- Network downtime: Rare but real, card network or issuer processing outages cause declines that are entirely unrelated to the account status.

Authorization failure rates vary by transaction type, but card-not-present transactions decline at materially higher rates than in-person swipe transactions, a gap that has widened as card security measures have become more aggressive.

Key Elements Every Credit Card Authorization Form Should Contain

A complete CCA form protects both the hotel and the company authorizing the charge. Missing fields are a common reason hotels refuse to process a form, and a reason why standardized templates matter.

A properly completed credit card authorization form must include:

- Cardholder’s full legal name (as it appears on the card)

- Card number (full or partial, per property policy)

- Card network (Visa, Mastercard, American Express, Discover)

- Expiration date

- Billing address and ZIP code

- CVV (where required, some properties request, others do not)

- Name of the hotel and reservation confirmation number

- Guest name and check-in/check-out dates

- Explicit statement of charges authorized (room rate, taxes, incidentals, or room and tax only)

- Cardholder signature and date

The scope of charges authorized is the most consequential field. A form authorizing “room and tax only” will not cover incidental charges, and if a traveler orders room service, the hotel may require a separate payment method at checkout. Travel managers at companies with tight expense policies should specify scope explicitly and communicate it to travelers before check-in.

Fixing the Authorization Process: Where to Start

The credit card authorization process is not broken by design. It is broken by the gap between how it was built, a cardholder-present, real-time transaction model, and how corporate travel actually works: centralized payment, remote travelers, and hotels that receive authorization instructions through whichever channel they’ve always used.

The companies that manage this well share three practices: they standardize their CCA form to cover the specific charges they authorize (not “all charges” as a blanket), they build a confirmation step into every authorization workflow rather than assuming sent equals received, and they treat the 24–48 hour virtual card window as a hard constraint that affects booking cutoffs, not a soft guideline.

For travel managers handling high volumes of hotel bookings, particularly in staffing, healthcare, or project-based industries where placements change frequently, manual CCA management at scale is genuinely unsustainable. ITILITE’s virtual card and authorization workflow is built specifically for this operating model: automating card issuance, transmitting authorization details directly to properties, and reducing the manual confirmation loop that currently falls on travel managers at the end of every booking.

If your team is spending meaningful time each week on credit card authorization forms, the question isn’t whether to fix it, it’s how quickly you can close the gap between the process you have and the one your travelers actually need.